{kind=link}

In recent days, the attention of global financial investors is focusing on one of the world’s largest banks Credit Suisse with speculation surrounding the story of bankruptcy risk. This bank has reassured investors and customers, but the stock still fell by 11% in the session of October 3 before recovering strongly and ending the session down nearly 1%. Since the beginning of the year, Credit Suisse stock has dropped 55%, corresponding to a capitalization of 10 billion USD, compared to 22.3 billion USD a year ago. Valuation also fell to a record low with a P/B of only 0.22x.

Not only Credit Suisse, but the valuation of many big banks in the world has also fallen below book value, such as Bank of America Corp, Goldman Sachs Group Inc, Wells Fargo & Co,… Even, P /B of a series of famous names such as Deutsche Bank AG, BNP Paribas SA, Citigroup Inc, Bank of China Ltd, Barclays PLC, Mitsubishi UFJ Financial Group Inc, Standard Chartered PLC, Sumitomo Mitsui Financial Group Inc,… below 0.5.

If only looking at the P/B figure, some Vietnamese banks even have valuations in the top “most expensive” in the world. According to data from SSI Research, banks such as Vietcombank (VCB), SeABank (SSB), Eximbank (EIB), National Citizen Bank (NVB) are all valued at more than twice the book value, especially VCB with a very high P/B of 2.75x.

In fact, recent adjustments have made the banking sector’s valuation “softer” relative to the beginning of the year. Median P/B 2022 is currently just 1.3x, 35% below the 3-year average of 2x. Most banking stocks have P/B below 1.5 times, even some names have fallen below book value, notably VietinBank (CTG), Sacombank (STB), SHB, LienViet Post Bank (LPB),… However, this valuation is still significantly higher than many big banks in the world.

Basically, all comparisons are lame and the banking industry in Vietnam has certain characteristics that make the market accept higher valuation grounds. One of them is the difference in operating types between Vietnamese and international banks, which could affect growth prospects in an environment of rising interest rates.

With the investment banking segment accounting for a large proportion, the “giant” banks in the world are considered to face many difficulties as the Fed accelerates the withdrawal of money, creating a wave of global capital withdrawal, negatively affecting the economy. investment channels. Meanwhile, Vietnamese banks are mostly commercial banks with credit activities still being the mainstay and the trend of increasing interest rates is assessed to have mixed effects.

Difficulties still surround

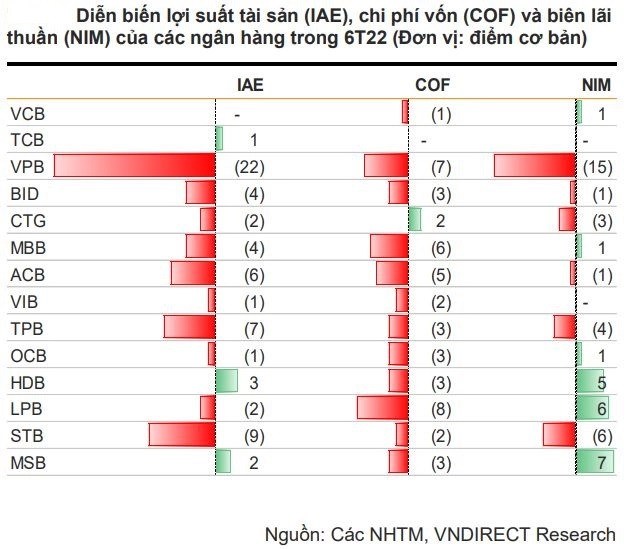

Recently, the State Bank of Vietnam (SBV) has decided to raise a series of operating interest rates and raise the ceiling deposit interest rate, but still keep the lending rate ceiling unchanged. If the output interest rate cannot be increased in proportion to the increased input deposit interest rate, the bank’s NIM will be pulled down. Besides, demand deposits (CASA) are also affected because cash flows on current accounts tend to look for term deposit channels with higher interest rates.

In addition, rising interest rates partly slow down economic growth and thereby affect the financial health of businesses as well as consumers. As the financial situation in households and economic organizations becomes increasingly difficult, the rising financial costs also contribute to higher bad debt.

However, according to some comments, in the context that the credit room of many banks is exhausted, the increase in loan interest is difficult to avoid. At the beginning of September, the SBV extended credit limits for 18 commercial banks. According to the new credit lines of these banks (accounting for 80% of system credit), VNDirect forecasts total credit growth will reach nearly 13% by the end of the year. With the primary goal of controlling inflation and stabilizing the macroeconomy, this securities company believes that it is unlikely that commercial banks will receive additional credit lines from now until the end of 2022.

In fact, interbank interest rates are increasing strongly in recent days even though the SBV has continuously used open market operations tools to maintain liquidity in the system. Currently, the overnight interest rate on the interbank market is at 5.71%/year; 3-month term is 6.13%/year; term from 9 months to 6.78%/year. This is the highest interest rate in the past 7 years.

Rong Viet Securities forecasts that lending interest rates will be under pressure of a strong adjustment in the second half of 2022 and into the whole of 2023 due to limited credit space, increased deposit interest rates, and insufficient liquidity in the system. due to the priority of exchange rate stability and inflation control.

Although it is not possible to accurately assess the impact of the interest rate increase on the business activities of banks, the impact on stock movements is quite clear. Cash flow into the stock market is relatively limited in the context of monetary tightening, which is forecasted to be difficult to absorb the huge amount of free-floating shares of the banking group.

Source: CafeF

Source: Vietnam Insider