{kind=link}

The first factor (blockade in China) puts downward pressure on prices, because China’s steel output may decrease due to some production shutdowns, such as Tangshan, as well as the ability to affect prices. affect economic growth.

The second factor (Russia and Ukraine) can put upward pressure on prices, which can also cause prices to decrease, depending on how the conflict between these two countries develops.

Both Russia and Ukraine are major steel exporters, with Russia exporting around 28 million tons/year in recent years, second only to Japan, although far behind the number one producer, China, which exports 52.63 million tons of steel products in 2021, according to official data.

Ukraine exports about 15 million tons of steel a year, ranking eighth and fifth largest exporter of iron ore in the world, although its volume is small compared with leading exporters Australia and Brazil.

According to research by Refinitiv, Ukraine exported 21.26 million tons of iron ore in 2021, or about 2.5% of the 884 million tons that Australia exported.

Since Russia carried out “Special Operation” in neighboring Ukraine on February 24, international customers have stopped buying the country’s steel, although it may take several months before the full impact of sanctions became apparent.

Ukraine’s iron and steel shipments have also been affected, as some major seaports are close to the conflict zones, making ship owners, insurance companies and traders reluctant to go through those ports.

This looks positive for iron ore and steel prices, as supply is likely to tighten, especially in Europe, which consumes most of its supply from Russia and Ukraine.

However, it could also cause Russian steel to shift more to Asia, as exporters seek new markets for products that are no longer bought by Europeans. That, once it happens, could shake up Asia’s steel market, especially if Russian products are heavily discounted and become much cheaper than products from traditional Chinese suppliers. regions, are China, India, Japan and Korea.

On the contrary, Asian exporters may find new opportunities to export to Europe, especially if European steel mills are constrained by rising energy costs, hindering their steel production activities. themselves.

Overall, the impact of Russia’s likely exclusion from much of the European steel market will also be felt in Asia, and a re-correction of trade flows is expected.

Much of those possibilities will also depend on China’s future steel demand, how long the country’s anti-Covid-19 blockade will last, and whether there is a subsequent increase in steel requirements. stimulus program (aggressive spending on infrastructure) or not, as Beijing tries to regain economic momentum.

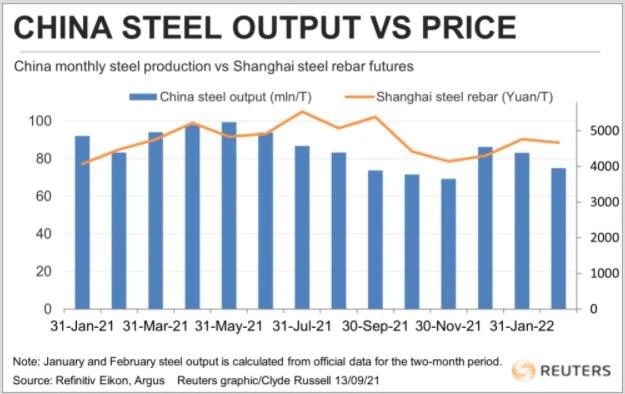

China’s steel production increased again?

Official data shows that China’s crude steel output fell 10% in the first two months of this year to 157.96 million tons, from 172.99 million tons in the same period in 2021.

Restricting production to reduce air pollution ahead of the Beijing Winter Olympics is part of the reason for the drop in output, but high iron ore and coke prices are also limiting efforts. factories in operation at high capacity.

China’s exports of steel products also declined in the first two months of the year, reaching only 8.23 million tonnes, down 18.8 percent year-on-year, according to customs data.

However, the start of the new year with low output and exports does not mean that the following months will continue to be so. And in fact, there are already some signs that China’s steel production is increasing.

China Iron and Steel Association said the country’s crude steel output in the 10 days to March 20 increased by 4.61% compared to the previous 10 days.

Amid the uncertain outlook for both China’s steel sector and the impact of the Russia-Ukraine crisis, the iron and steel market is trading in a very cautious manner, keeping prices from being volatile as much as the market. oil and natural gas, although “underground waves” are not inferior.

The price of 62% iron ore imported into China was reported by commodity quotation agency Argus at $146.40 per tonne on Thursday (March 24), up slightly from $137.20 on May 23. 2, the day before the Russian-Ukrainian conflict.

The price of rebar futures on the Shanghai Futures Exchange on March 24 ended at 4,976 yuan ($782) per tonne on Thursday, up from 4,775 yuan on February 23.

The modest price gains for both iron ore and steel in Asia reflect market concerns about the economic stimulus from China (push up prices) and the loss of export supply due to the crisis in Asia. Ukraine will ultimately be resolved.

China steel output and price.

Reference: Refinitiv

Source: Vietnam Insider