In a prior piece discussing JPMorgan Chase & Co., the term “Morganization” was introduced, signifying a strategy aimed at fostering the Merger & Acquisition market by providing comprehensive consulting services and information for companies seeking M&A deals.

This trend underscores the increasing significance of entrepreneurship for the future prosperity of the US economy. Today, we delve into the historical backdrop of the M&A market, tracing its roots back to the pioneering efforts of tycoon John Davison Rockefeller Sr. (1839-1937), who established the first-ever trust fund – Standard Oil.

Our journey takes us to the 1850s, a period witnessing the emergence of the petroleum industry fueled by the discovery of refined petroleum’s utility for lamp oil. Subsequently, the industry experienced rapid expansion, with oil companies proliferating and oil wells springing up, particularly following significant discoveries in Pennsylvania and the Midwest. Post the Civil War (1861-1865), a novel business organization emerged in the form of trust funds, with John Davison Rockefeller Sr. founding the inaugural trust company, Standard Oil, in 1870. These trusts, structured to allow a third party or trustee to manage assets on behalf of beneficiaries, aimed at curbing competition.

By the late 1860s, Rockefeller Sr. had consolidated control over oil refining in Cleveland, Ohio, leveraging advantageous rail rates and strategic maneuvers that pushed competitors out of the market.

In 1870, amidst the formation of Standard Oil, kerosene was priced at $0.26/gallon. By 1872, Standard Oil commanded over a quarter of the industry’s total daily capacity. Yet, challenges loomed as the company grappled with resistance from refiners, competition from railways, and regulatory hurdles.

The completion of the Tidewater pipeline in 1879 spelled trouble for Standard Oil, escalating crude transportation costs and necessitating a restructuring of its operations. By 1880, the company managed to slash kerosene prices to $0.09/gallon.

In 1882, learning from the Tidewater debacle, Rockefeller Sr. initiated the Standard Oil Trust Agreement, establishing a centralized joint stock agency to oversee 40 subsidiaries. This maneuver birthed the Standard Oil Trust, enabling the circumvention of state laws and the consolidation of control over subsidiaries, with headquarters relocating to New York.

The late 19th century witnessed the ascendancy of corporate behemoths dominating the American economy and dictating product prices, prompting public outcry against trusts and monopolies, and clamors for regulatory intervention. In 1890, amidst plummeting kerosene prices ($0.07/gallon), Standard Oil’s dominance persisted, facilitated by competitive advantages, vertical integration, relentless innovation, and strategic M&A maneuvers, capturing over 90% of the oil refining market share for over two decades.

Recognizing the pivotal role of oil in American life, Rockefeller Sr. wielded his influence to dictate oil prices, prompting public outrage. In response, President Benjamin Harrison (1833–1901) passed the Sherman Antitrust Act in 1890, aimed at curbing trusts, monopolies, and oligopolies, promoting fair competition, and regulating interstate commerce.

During President Theodore “Teddy” Roosevelt Jr.’s tenure, dubbed the era of “Breaking Trust,” stringent enforcement of the Sherman Act ensued, marked by over 40 lawsuits targeting monopolies and self-serving trusts. While Roosevelt acknowledged the potential benefits of trusts, he advocated for their regulation, although federal licensing and regulatory proposals faced congressional opposition.

100vw, 1170px” data-recalc-dims=”1″></p>

<p id=)

100vw, 1170px” data-recalc-dims=”1″></p>

<p>On May 15, 1911, the government ordered the breakup of Standard Oil into 34 smaller entities, marking a historic milestone as the first trust company subjected to dissolution. Today’s prominent oil companies, including BP, Chevron, ExxonMobil, Marathon, Shell Plc, and ConocoPhillips, trace their origins back to Standard Oil. Notably, Saudi Aramco, initially associated with the Kingdom of Saudi Arabia (KSA), originated from Standard Oil’s California branch, which entered into a joint venture agreement and concession pact with KSA in 1933 before being fully repurchased in 1980.</p>

<p>In 1914, drawing insights from the Standard Oil case, President Thomas Woodrow Wilson (1856-1924), nicknamed “Professor Federalism,” established the Federal Trade Commission (FTC) to counteract unlawful practices like fraud and deception. Building on the Sherman Act’s provisions against anticompetitive and monopolistic behaviors, Wilson enacted the Clayton Act, championed by Alabama Congressman Henry D. Clayton Jr. (1857-1929), which addressed specific concerns such as price discrimination, contractual obligations, and interlocking directorates. Moreover, the Clayton Act safeguarded workers’ rights, shielding them from employer-led legal challenges.</p>

<p>Rockefeller Sr. spearheaded the evolution of the trust fund model and spurred Congress to pass the Sherman Act to curb monopolistic tendencies. Reflecting on the M&A industry’s historical trajectory, the period spanning 1895 to 1904 witnessed a surge in horizontal mergers as businesses aimed to fortify their market positions in response to surplus capacity from prior economic downturns. As detailed in previous discussions, figures like J.P. Morgan played pivotal roles in the formation of General Electric in 1892, as well as the establishment of U.S. Steel and DuPont toward the end of the Gilded Age. Subsequently, heightened governmental oversight and regulation ensued to safeguard fair competition and forestall monopolistic consolidation.</p>

<div id=)

{kind=link}

Between 1925 and 1929, corporations pursued a vertical merger strategy, extending their influence from upstream suppliers to downstream distributors, consolidating dominance across sectors like finance, steel, automotive, rail, utilities, and consumer goods. The era was characterized by speculative fervor, spurred by inexpensive stocks with P/E ratios below five, propelled by robust industrial growth and emerging technologies such as radio and electricity. Cultural phenomena like Jazz and the allure of the Gatsby era further buoyed optimism. However, widespread stock market speculation, facilitated by margin trading and negligible interest rates, culminated in the market frenzy of the 1920s, led in part by figures like J.P. Morgan. This era of exuberant consolidation came to an abrupt halt with the onset of the Great Depression, marking the end of an era characterized by rampant consolidation and redundancy.

Post-Depression, the enactment of the Robinson-Patman Anti-Price Discrimination Act of 1936 aimed to curb price discrimination by prohibiting sellers from charging varying prices to different buyers for the same product. In 1950, the Celler-Kefauver Anti-Merger Act expanded restrictions on M&A activities aimed at stifling competition and fostering monopolistic control through asset and share acquisitions. Concurrently, economist Orris C. Herfindahl refined the concept of quantifying market concentration initially proposed by German economist Albert O. Hirschman. This refinement gave rise to the widely utilized Herfindahl-Hirschman Index (HHI), employed by entities like the Department of Justice (DOJ) and FTC to gauge market concentration levels. See the accompanying image for an interpretation table of the HHI.

Between 1965 and 1970, businesses found ways to navigate legal constraints by diversifying their investments, giving rise to a new corporate model known as the conglomerate. Over the preceding five years, M&A activities gained traction as a means to diversify business operations and mitigate risks posed by antitrust regulations. The 1960s were marked by robust economic growth and optimism, evidenced by surging stock prices and heightened investor confidence. Among the prominent players during this era was ITT Inc., which expanded its reach by acquiring multiple telecommunications, electronics, and aerospace firms, capitalizing on economies of scale, cross-selling opportunities, and risk mitigation. This trend prompted management and regulatory agencies to remain vigilant against emerging forms of monopolies.

In 1976, Congress passed the Hart-Scott-Rodino Antitrust Improvements Act, mandating that companies embarking on significant M&A endeavors notify the FTC and DOJ beforehand, considering potential antitrust implications.

From 1984 to 1989, the corporate landscape witnessed widespread financial activity through hostile takeovers and debt-financed transactions, particularly leveraged buyouts (LBOs). Deregulation, financial innovation, and favorable economic conditions fueled a bustling M&A market. Hostile takeovers gained prominence as aggressive firms sought to acquire undervalued entities, often bypassing management resistance by directly engaging shareholders. A notable instance was the monumental $25 billion LBO orchestrated by Kohlberg Kravis Roberts (KKR) against RJR Nabisco in 1988, later immortalized in the movie “Barbarians at the Gate.” Additionally, Wall Street witnessed the advent of high-yield “junk” bonds championed by Michael Robert Milken to finance LBOs amid declining macroeconomic interest rates and a bullish stock market. However, escalating debt levels led to widespread restructuring and layoffs, prompting a reevaluation of corporate practices to foster sustainable development.

100vw, 1170px” data-recalc-dims=”1″></p>

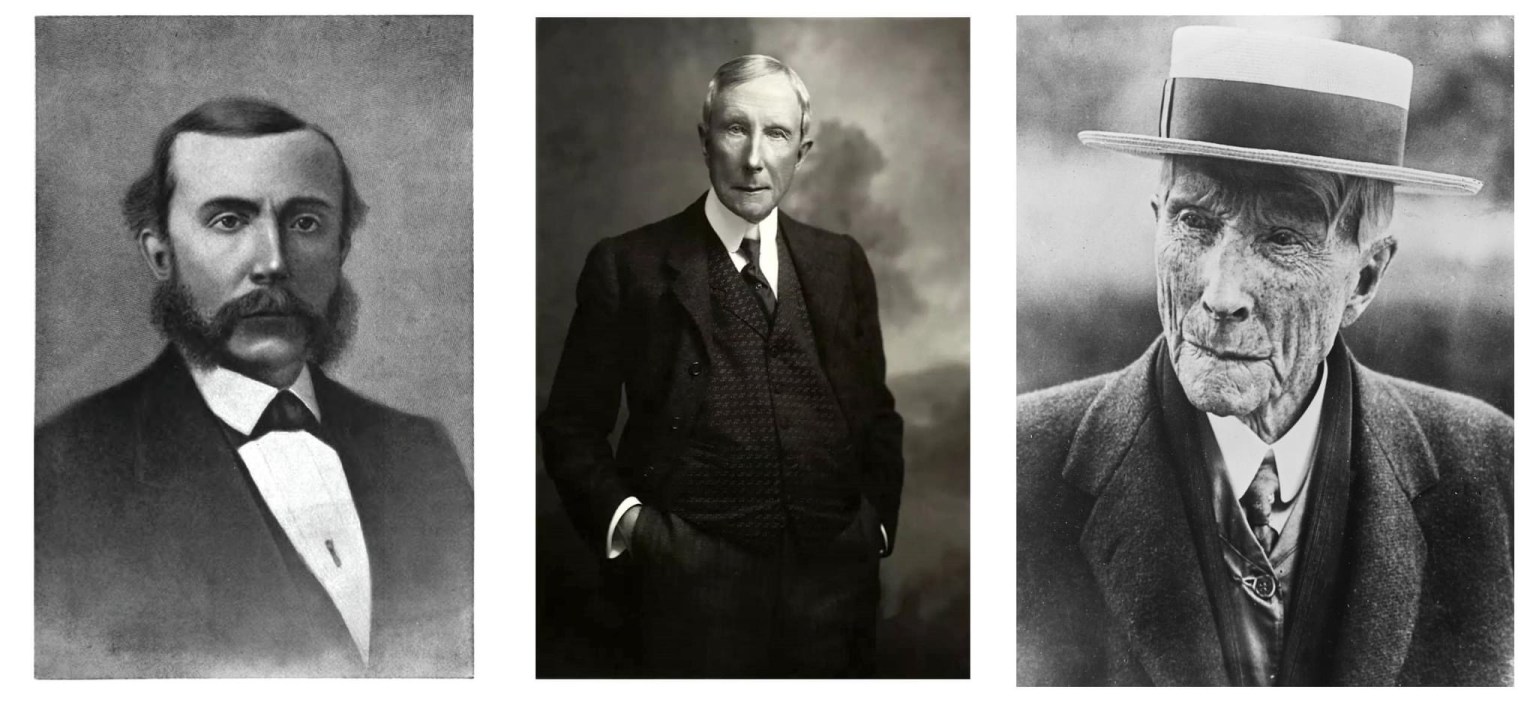

<p id=) Left to right: Rockefeller, 33 years old, Founder at Standard Oil; Rockefeller 75 years old, and Rockefeller 83 years old

Left to right: Rockefeller, 33 years old, Founder at Standard Oil; Rockefeller 75 years old, and Rockefeller 83 years old

From 1994 to 2000, the business landscape underwent a transformative “paradigm shift,” marked by strategic and game-changing M&A transactions that reshaped entire industries. Notably, the $164 billion merger between AOL and Time Warner Cable in 2000 epitomized this trend, catalyzing advancements in media and the internet, revolutionizing content production, distribution, and consumption. Rapid advancements in information technology, coupled with globalization, dismantled trade and investment barriers, fostering cross-border collaboration and creating opportunities for emerging technology firms to participate in the M&A arena. While this era witnessed speculative excitement and the subsequent burst of the dot-com bubble in the early 2000s, it laid the groundwork for the digital revolution and reshaped the global economy in the years to come.

From 2004 to 2008, globalization propelled the world economy forward, driven by advancements in technology, communication, and trade liberalization. If the 1960s heralded the emergence of the corporate model, this era witnessed the rise of multinational corporations expanding their operations across borders, capitalizing on emerging markets and leveraging global supply chains to foster economic growth and efficiency. Regulatory bodies such as the DOJ and FTC collaborated with international antitrust agencies like the European Commission and the Japan Fair Trade Commission to address anti-competitive practices on a global scale. Concurrently, the Federal Reserve (Fed) adopted accommodative monetary policies, including a zero-interest-rate policy and the infusion of liquidity into financial markets, fueling a credit bubble. Financial institutions expanded subprime mortgage lending, contributing to unsustainable debt levels and speculative frenzy in the real estate market. Amidst this backdrop, leveraged buyout (LBO) activities surged, with private equity funds capitalizing on cheap financing to acquire and restructure companies for short-term gains. Notably, the acquisition of TXU Corp by KKR, Texas Pacific Group, and Goldman Sachs for $45 billion in 2007 exemplified this trend. However, the euphoria came crashing down with the onset of the global Great Recession in December 2007, triggered by the collapse of the subprime mortgage market and the unraveling of collateralized debt obligations. The recession laid bare the fragility of the financial system, leading to bank failures, a precipitous decline in stock markets, and widespread unemployment. While this period was marked by prosperity and excess, it prompted a critical reevaluation as the global economy grappled with the aftermath of unsustainable debt and financial instability.

Between 2014 and 2022, the global economy underwent a phase of capacity rationalization and strategic consolidation across diverse industries. Companies streamlined their operations, enhancing efficiency and production capacity to adapt to market dynamics and competitive pressures. This period witnessed a flurry of strategic M&A deals aimed at scaling up and bolstering competitiveness. Post-Great Recession, the Fed pursued accommodative monetary policies to spur economic recovery, fueling a surge in M&A activity, particularly in the technology, healthcare, and consumer goods sectors. In 2023, Microsoft’s acquisition of Activision Blizzard raised antitrust concerns, highlighting the need for stringent regulatory oversight to ensure fair competition, especially given Microsoft’s dominant position in the gaming industry through its Xbox platform and game services. While the technology sector thrives, heightened government scrutiny necessitates vigilance among large enterprises to avoid inadvertent violations.

The M&A market boasts a storied history, fraught with challenges and unintended consequences. Regulatory agencies must enhance legal frameworks to govern consolidation practices and uphold ethical standards to prevent the unchecked consolidation of market power. Frontier and developing markets stand to benefit from this model by bolstering legal certainty and fostering sustainable economic development in the future.

Related

Source: Vietnam Insider